admin | Apr. 13, 2019

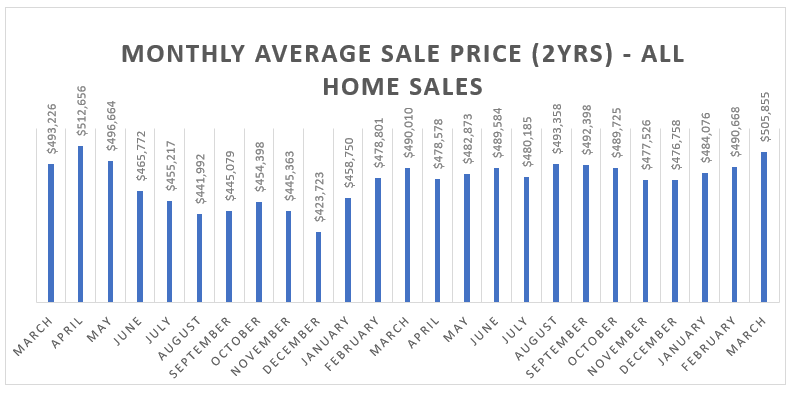

There were 511 homes sold in March, with Sales dipping 5.7% vs the same period in 2018 and were 7% below the 10-year average. The average price in March was up 3.2% at $505,855 vs March 2017. The average price of homes is being driven by competition for homes under $500,000 and to a smaller extent by homes $500,000 to $600,000. Demand in these price ranges is high and supply is low. This supply/demand dynamic is putting upward pressure on home prices in those ranges even with slowing sales.

All homes: $505,855 Up 3.2%

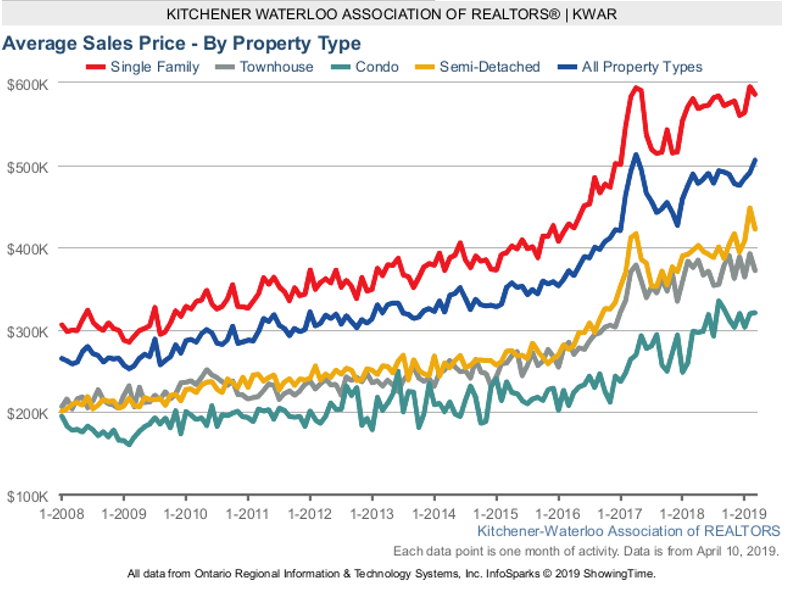

Single detached homes: $585,668 Up 0.8%

Apartment Condos: $320,857 Up 7.5%

Townhouses: $372,003 Down 1%

Semi-detached: $422,360 Up 6.4%

511 Total Sales Down 5.7%

325 Singles detached homes sold Up 3.2%

45 Apartment style condos sold Down 11.8%

116 Townhouses sold Down 14.7%

25 Semi-detached homes sold Down 37.5%

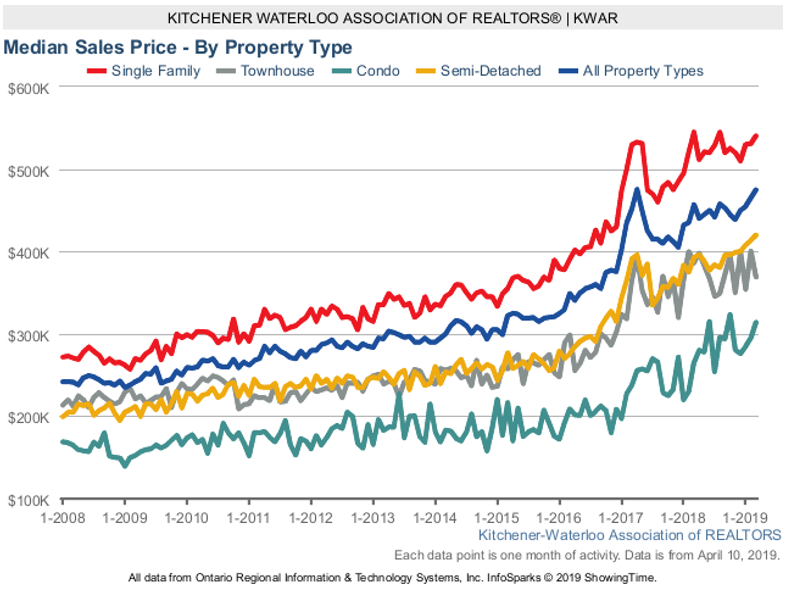

Below we can see the yellow ($500k+) and green ($400k – $500k) lines becoming very dominant as homes prices under $400,000 are almost extinct in KW.

The below chart shows the average price trend over the last two years and as usual we are seeing our spring average price spike. We are currently sitting above last years prices and slightly below the 2017 April peak. It will be interesting to see what the average price does in April – We have seen some strength in higher priced homes since April 1st.

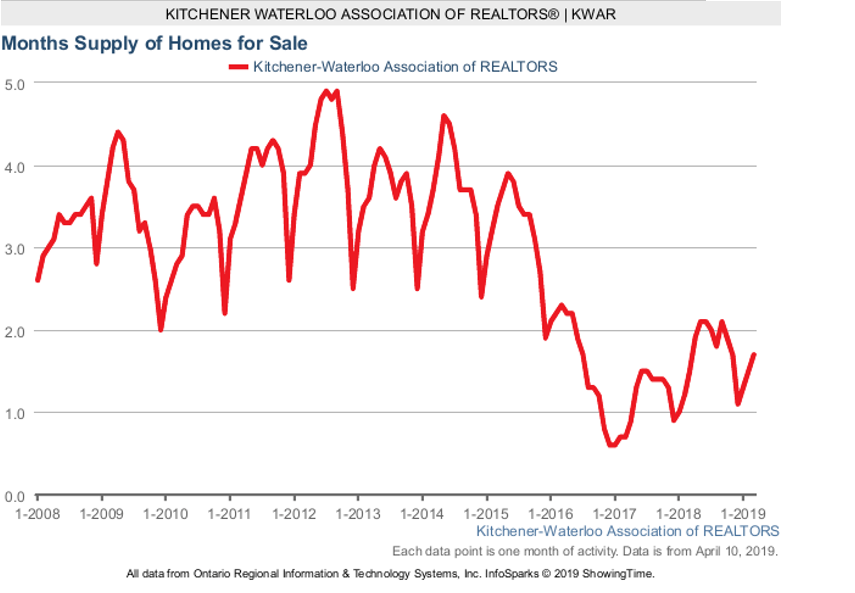

The below data solidifies the fact that homes under $600,000 are driving this market. Average price is up along with the median price. Sales are down while overall active supply on MLS at the end of March was actually up 5.4% vs last year and this is for a month where we saw 4.8% fewer listings posted.

Continuing with my pessimistic tone from last month, I think it means that there will be a reversion to a normal market. If the market is dominated by Buyers in the $500,000 range and the demand for homes priced there keeps pushing those prices up then eventually you will see some of those Buyers give up as they get priced out of the market. This will eventually create equilibrium especially given the tightening in credit which has put some hard ceilings in place for the amount of money the Banks are willing to lend. The Banks in Canada are currently being scrutinized. Their exposure has some people concerned and some people licking their chops betting that they are going to see hard times ahead. Steve Eisman – the portfolio manager who called the financial crisis and immortalized by the book and movie “The Big Short” – has initiated short positions on some of Canada’s banks. He’s not calling for a Financial Crisis 2.0, but rather normalization of credit losses or basically a reversion back to a normal amount of people defaulting on their loans. I tend to agree with him. Credit has been very easy for years and Canadians used that credit to buy homes and drive up home (asset) prices. As long as home appreciation kept going then the environment works because Canadian debt to asset ratios were kept low as their asset (home) values kept rising.

If you got into some trouble you could sell your home for a profit or simply refinance or pull money out of your home. Stricter mortgage and borrowing rules and Canadian banks being put under a microscope causing them to tighten up, is slowing sales and home price appreciation. It looks like we are nearing the end of a credit cycle or to be clear, Canadians have borrowed so much that we can’t borrow any more. Canada’s debt-to-GDP ratio of 100% and debt to disposable income of 170% are the highest in the Global north. I think the banks are very aware of our debt levels and what happened in the US when the financial crisis caused mass deleveraging. Over the last 6 months TD bank has been very difficult to deal with in terms of mortgage approvals. They want to reduce their exposure.

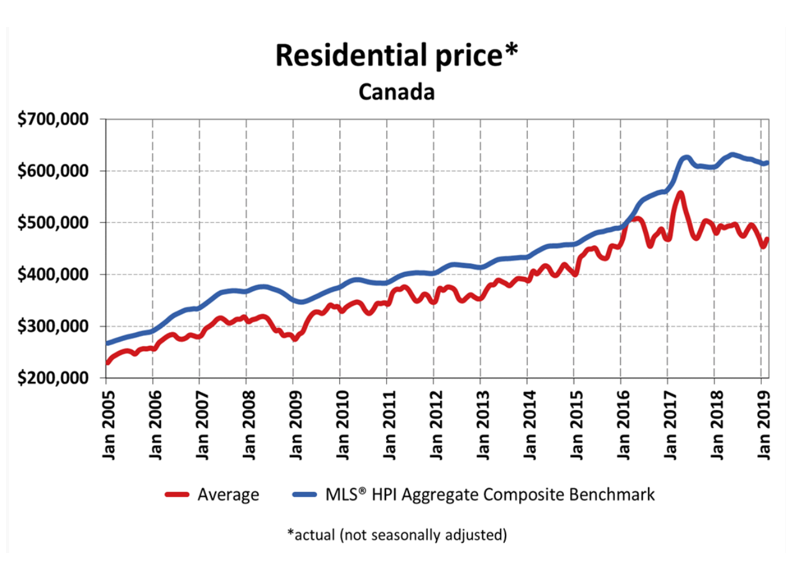

I was speaking with a Mortgage agent from TD and he noted that TD is shying away from higher risk mortgage exposure – namely mortgages on rental properties and the like. Is this prudence or are they worried about something? Given that wages in Canada have risen from about $20.50 in 2009 to about $25.50 in 2019 we have seen a rise of about 24%. The average home price in Canada has risen from about $280,000 in 2009 to about $475,000 today representing a 70% increase. How can we even afford homes? Credit baby! Except that the ice cream truck of credit may be running out of popsicles.

The end of a credit cycle doesn’t mean the world ends. It doesn’t mean that anything bad has to happen at all. It just means that we should adjust our expectations. Rather than close your eyes and buy we take a more calculated and cautious approach. In a low growth environment there will be opportunities. And keep in mind that there will be a return to accelerated growth in the future. There are and will be opportunities in the Real Estate market – We will be able to buy homes without competing with other Buyers and we will be able to pick up distressed properties and score huge: The best time to buy is when everyone else is selling.

I’m probably wrong – I hope I am and the world just keeps on trucking and we can keep buying shiny stuff and taking nice vacations. But, in case the truck stalls a bit then it might be wise to take a position now that allows for flexibility to take advantage of any opportunities that require some cash or requires strong credit – because if I am right, those shiny things and nice vacations may just turn into VERY shiny and VERY nice.